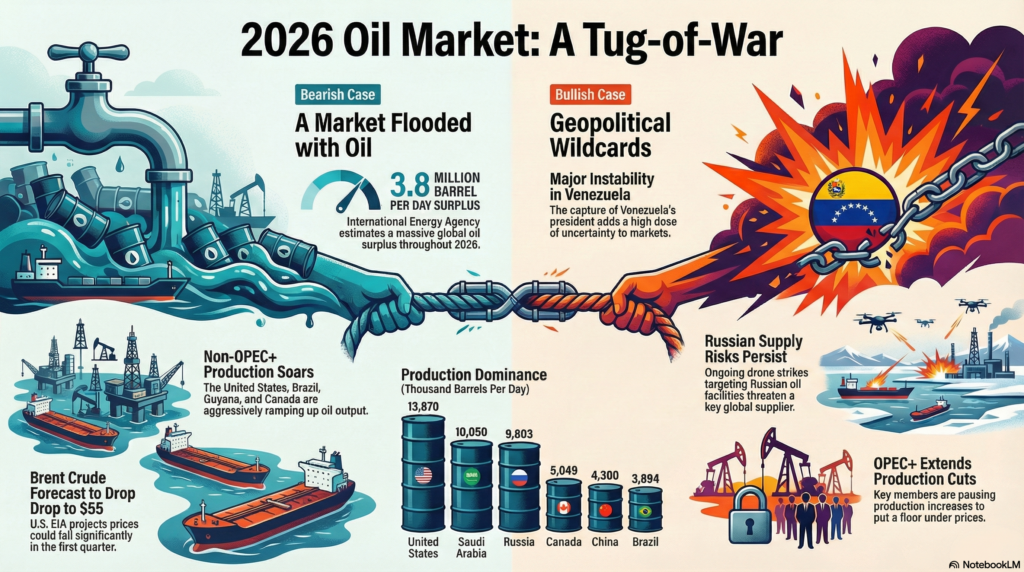

As we enter the first weeks of 2026, the global oil market finds itself caught in a dramatic struggle between deeply entrenched bearish fundamentals and sudden, explosive geopolitical shocks. Following a tumultuous 2025 that saw oil prices log their steepest annual decline since 2020, the new year has begun with a complex narrative that is keeping traders and analysts on edge. The overarching theme remains one of structural oversupply, yet headline-grabbing political events across the globe are preventing a complete price collapse, creating a volatile and uncertain landscape for energy markets.

The primary driver of market sentiment continues to be the relentless growth in global oil production, which is outpacing the rise in consumption. Forecasts from major energy agencies paint a clear picture of a well-supplied market. The U.S. Energy Information Administration (EIA) has projected that Brent crude prices could fall to an average of $55 per barrel in the first quarter of 2026, a significant drop from the levels seen just a year ago. This downward pressure is largely fuelled by robust output from non-OPEC+ nations. Countries like the United States, Brazil, Guyana, and Canada are aggressively ramping up production, contributing to a substantial surplus that the International Energy Agency estimates could reach nearly 3.8 million barrels per day throughout the year. This flood of new oil is causing global inventories to swell, acting as a persistent anchor on prices. On the demand side, growth remains tepid, driven primarily by non-OECD economies in Asia, while consumption in developed nations shows signs of stagnation.

However, this bearish backdrop has been aggressively challenged by a series of geopolitical thunderclaps in the opening days of January. The most significant development was the stunning news of U.S. military action resulting in the capture of Venezuelan President Nicolás Maduro. This event has injected a fresh dose of uncertainty into the market. While some analysts believe a more pro-Western government could eventually unlock Venezuela’s vast oil reserves and add millions of barrels to global supply by the end of the decade, the immediate reality is far more complex. The country’s dilapidated infrastructure means any significant production increases are likely years away, and the short-term effect has been to add a risk premium to prices due to the potential for instability. Meanwhile, ongoing drone strikes targeting Russian oil facilities as part of the continuing war with Ukraine serve as a constant reminder of supply risks in other key regions. These geopolitical flashpoints have caused prices to stage modest rallies, briefly pushing Brent back above the $60 mark in early trading.

In response to this evolving landscape, the OPEC+ alliance has opted for a cautious approach. In a crucial meeting on January 4, 2026, eight core members of the group agreed to extend their existing pause on production increases through February and March. Citing seasonal demand fluctuations and the paramount need for market stability, key producers like Saudi Arabia and Russia are aiming to counter the prevailing oversupply narrative and put a floor under prices. They have retained the flexibility to gradually unwind these voluntary cuts depending on market conditions, a strategy described as a careful balancing act in the face of global market fluctuations. This decision reflects the group’s acute awareness of the delicate equilibrium they are trying to maintain.

Looking ahead, the oil market in early 2026 is poised on a knife-edge. The fundamental reality of rising non-OPEC+ supply and building inventories points to lower prices ahead. Yet, the world remains a deeply unstable place, and as recent events in Venezuela have demonstrated, geopolitical shocks can strike with little warning, momentarily upending market logic. For now, the market is a battleground where the weight of surplus barrels is being constantly tested by the unpredictable nature of global politics.

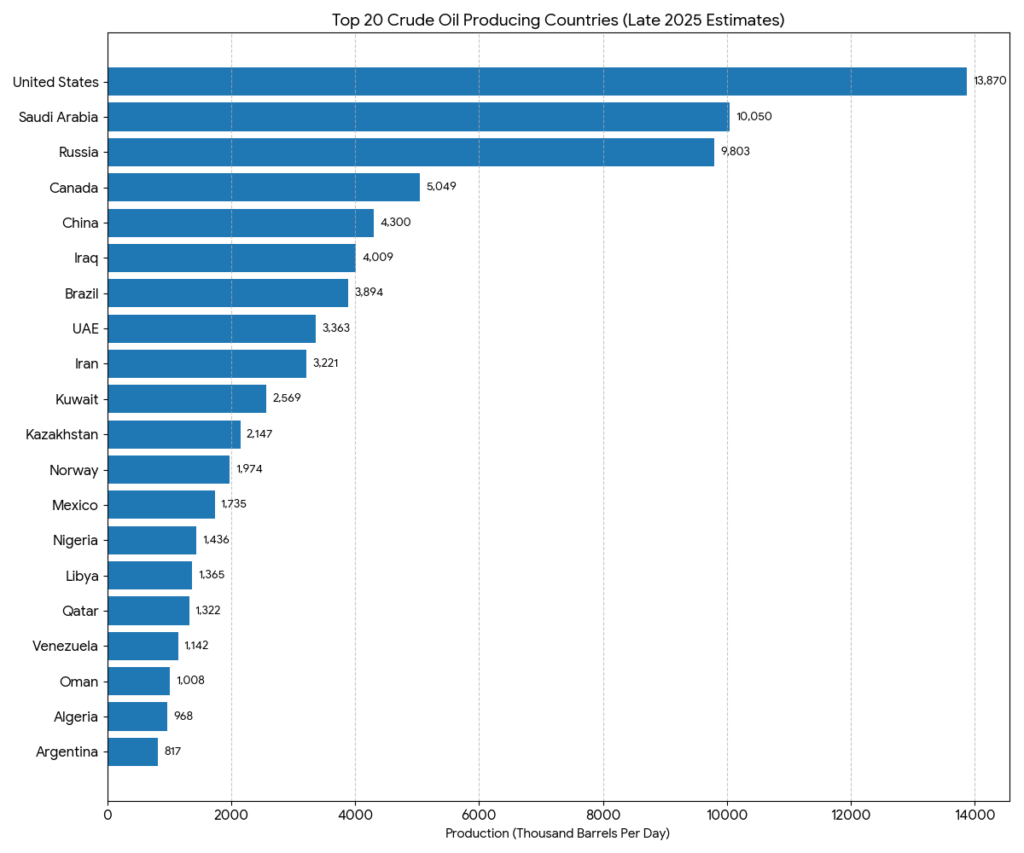

Top 20 Crude Oil Producing Countries (2025/2026 Estimates)

The chart below visualizes the production disparity, with the “Big Three” (United States, Saudi Arabia, and Russia) maintaining a significant lead over the rest of the world.

Production Data (in Thousand Barrels Per Day)

- United States: 13,870

- Saudi Arabia: 10,050

- Russia: 9,803

- Canada: 5,049

- China: 4,300

- Iraq: 4,009

- Brazil: 3,894

- United Arab Emirates: 3,363

- Iran: 3,221

- Kuwait: 2,569

- Kazakhstan: 2,147

- Norway: 1,974

- Mexico: 1,735

- Nigeria: 1,436

- Libya: 1,365

- Qatar: 1,322

- Venezuela: 1,142

- Oman: 1,008

- Algeria: 968

- Argentina: 817

Note: Figures represent Crude Oil production (excluding biofuels and natural gas liquids). Data reflects the latest available monthly estimates from late 2025.

Detailing the production dynamics of these key countries in the 2026 landscape.

The dominance of the “Top 3″—the United States, Saudi Arabia, and Russia—continues to be the backbone of the global market, but with diverging strategies that define the price per barrel. The United States, consolidated as the world’s largest producer at 13.87 million barrels per day (bpd), drives the global oversupply through continuous efficiency in the Permian Basin and sector deregulation. In contrast, Saudi Arabia and Russia, while maintaining massive volumes near 10 million bpd, operate under the constraints of OPEC+. While the Saudis seek to defend a price floor through voluntary cuts, Russia faces the additional challenge of drone attacks on its refineries and Western sanctions, making its actual output a constant element of volatility and geopolitical uncertainty.

In the middle tier, Canada and Brazil emerge as the great engines of growth outside the OPEC+ coalition, challenging the market control of traditional producers. Canada, at 5.04 million bpd, has benefited from the expansion of the Trans Mountain pipeline, which finally allowed oil from Alberta’s oil sands to reach global markets with greater ease. Brazil, reaching the historic mark of 3.89 million bpd, has consolidated itself as a pre-salt powerhouse. The commencement of operations for new Floating Production Storage and Offloading (FPSO) units in the Búzios and Mero fields has not only elevated Brazil to the position of the largest producer in Latin America but also made it a strategic ally for countries seeking to diversify their supply sources outside the Middle East.

The dynamics between China and Iraq illustrate the balance between voracious consumption and infrastructure dependency. China maintains a stable production of 4.3 million bpd, but its primary focus in 2026 has been strategic storage, taking advantage of low prices to stockpile massive reserves. Meanwhile, Iraq, producing around 4 million bpd, remains the “X-factor” within OPEC+; the country struggles to balance its desperate need for revenue for national reconstruction with pressure from the group to adhere to production quotas. Together, these seven nations control the rhythm of the global economy, where any technical disruption in Canada or a new political jolt in Iraq can instantly nullify surplus supply projections.